Overproduction has been fashion’s constant companion for years. For a long time, overproduction was financially feasible due to (inhumanely) cheap raw materials, labour, and transport. Combined with high mark-ups, fashion found a way to make overproduction profitable, albeit at a great environmental expense.

And the latter is becoming more imminent. According to the Paris Agreement, brands and retailers have to reduce their production emissions by 45% in 2030. That’s just six years away. Decarbonisation is no longer merely a nice marketing tool, it’s now a legal obligation.

Production emissions can be reduced through two ways:

- more sustainable (material) production

- lower production volumes

For a long time, the focus for making the fashion industry more sustainable has been on better (material) production. And rightfully so, material production is responsible for circa 45% of a garment’s total life cycle emissions. But what is often overlooked in sustainability analyses is the decarbonisation effect of reducing (over)production. The reason so little research has been done into this is because degrowth in production levels is widely associated with degrowth in margins. And that is a blatant misconception.

It’s time to assess both the cost- and carbon- effectiveness of reducing overproduction for the apparel industry at large. But first, we need to get a tighter grasp on overproduction.

1. Quantifying Overproduction

In order to estimate the size of the decarbonisation opportunity associated with minimising overproduction, it is first necessary to define and quantify the level of overproduction. Overproduction is a widely used term in the fashion industry and while many agree that it is estimated at around 30%, no one seems to have a clear cut definition of what overproduction actually entails, which makes the 30% more of a guessing game, and less of a reliable estimate. The reason so little data on overproduction is available, is due to several factors:

- (Unsold) inventory is hard to keep track of for brands, so most brands don’t actually know how much they overproduce. ‘Due to factors like counting errors, mistakes in packing and shipping, misplaced items and theft, retailers can have surprisingly poor knowledge of what stock they’re holding, with studies finding accuracy levels of around 50 percent or less in some cases’.

- Overproduction and subsequent garment destruction are dirty words in the fashion industry, especially since (amongst others) Burberry was caught destroying unsold goods. Ever since, brands aren’t so keen on disclosing:

- How much they over produce

- What happens with these unsold garments

- Overproduction also has a seemingly undefined scope. Does it just include garments that haven’t been sold by the end of the season? And what about garments that are sold, but returned, restocked and never sold again? Or garments that are sold, returned, and not restocked but immediately sent to landfill? And what about garments that end up in outlets? Or unsold garments that are sold to liquidators or donated? Are any of these garments included in the dead stock analysis? We just don’t really know.

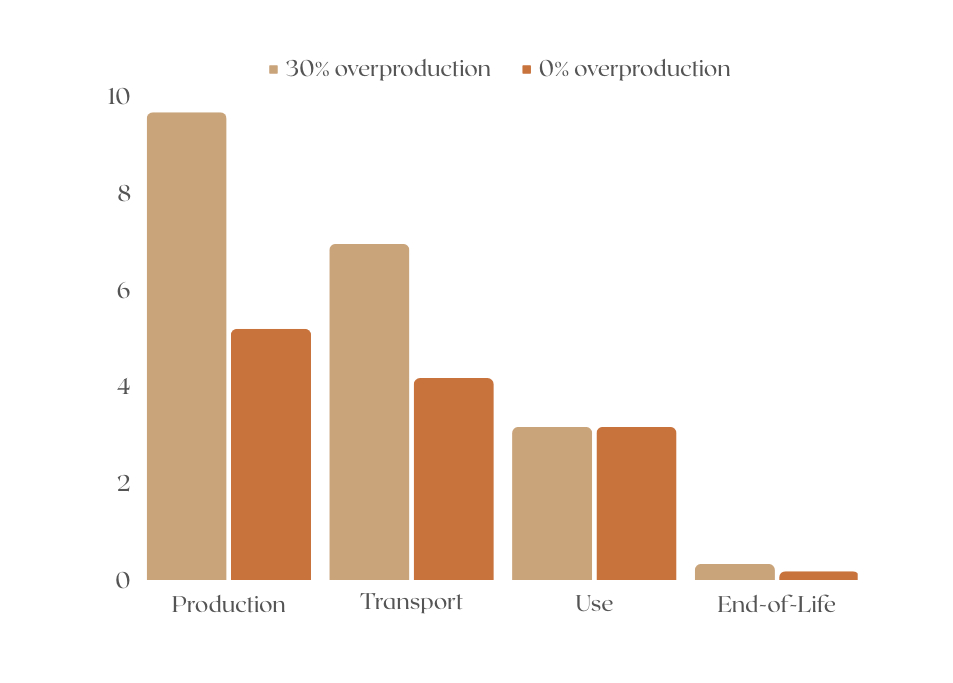

Up until now, it was estimated that global production volume is somewhere between 50-150 billion garments per year. However, according to Statista, in 2022, 170 billion garments were sold. Suggesting much more has actually been produced:

Tech Tailor’s analysis demonstrates that production volume is more likely to be around 276 billion garments per year. And when we account for secondary overproduction (e.g. unsold returns), overproduction rises to 38%. Meaning the industry output level estimates (and up until now, also our own) are off by approximately 125 billion garments.

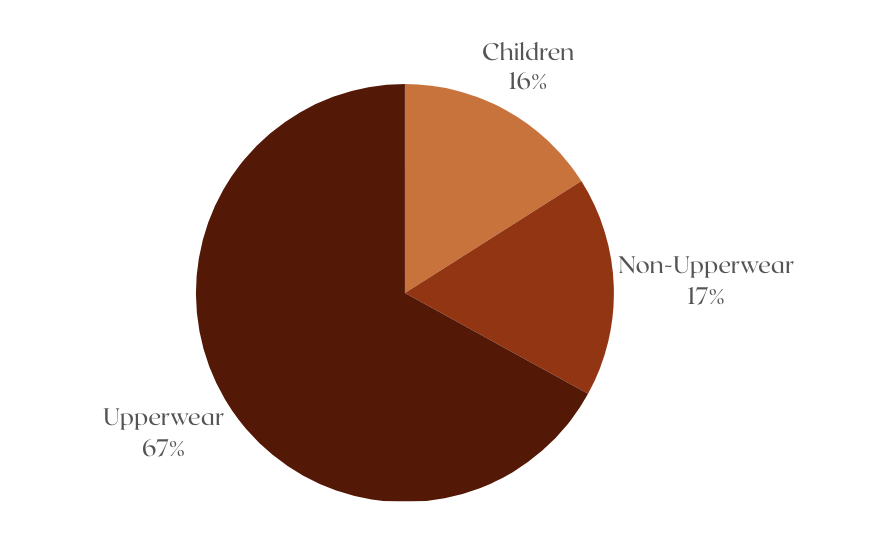

Additionally, it is important to note that not all overproduction is created equally. Apparel is roughly split up in three categories; children’s garments, non-upperwear (underwear, socks, ties, tights, etc.), and upperwear (shirts, trousers, dresses, coats etc.).

It can be assumed that overproduction is higher for upperwear than non-upperwear, due to two factors:

- Lower initial overproduction non-upperwear: Seasonality, evergreen, never out of stock etc.

- Lower secondary overproduction non-upperwear: Returns not allowed or less common due to lower fit criticality (socks, ties etc.)

2. The Environmental Impact of Reducing Overproduction

Reducing overproduction doesn’t just affect the emissions from the garments that were unnecessarily produced, it also affects the transportation emissions of garments that were unnecessarily shipped and the end-of-life emissions from garments that were unnecessarily destroyed.

Eliminating initial upperwear overproduction would theoretically decrease emissions for the total life cycle per upperwear garment sold by a staggering 37%.

3. Overproduction Reduction Methods

Admittingly, eliminating overproduction in its totality is somewhat impossible. However, brands can significantly reduce overproduction. We’ll look into three overproduction reduction methods: Better Sales Forecasting, Made-to-Order (MTO) and Made-to-Measure (MTM). For the purpose of a fair comparison, it is assumed that returns are allowed for both Made-to-Order (MTO) and Made-to-Measure (MTM).

3.1 Better Sales Forecasting

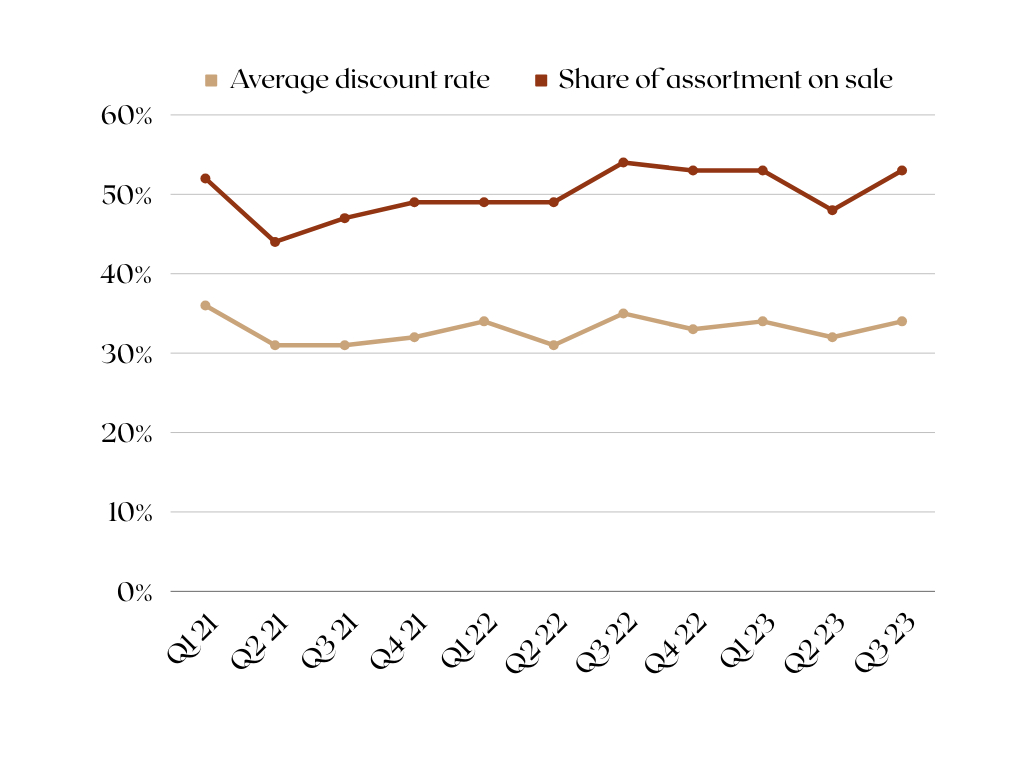

Better Sales Forecasting is the most popular overproduction reduction method, but unfortunately also the least effective one. Edited’s Retail Dashboard shows how online retailers are dealing with excess inventory:

Over the past three years around 50% of retailer’s online offerings have been on sale for an average discount rate of 33%. At the same time, retailer’s inventory has been outgrowing sales. So while sales forecasting has supposedly gotten more advanced, overproduction has gotten worse. We’re not even going to do the decarbonisation maths on this one.

3.2 MTO Produces On-Demand, in Standard Sizes

Now, on-demand production (MTO) is actually a very promising solution. If brands only produce what is actually sold, overproduction could become obsolete.

When near-shored, MTO could be 38% less polluting than RTW, for the whole life cycle of the upperwear garment. While MTO solves for inventory, it doesn’t solve for online returns. MTO provides customisation, but still produces in standard sizes. 70% of online returns are due to incorrect fit. So either brands have to deal with custom returns that can’t be resold, or customers can’t return their order, making them more hesitant to order in the first place. Both put pressure on this method.

3.3 MTM Produces On-Demand, Made-to-Measure

MTM solves the biggest pain point in the MTO model: sizing. Until now, tailoring is mostly used for high-end traditional formal wear. But with new technologies, it’s possible to produce MTM for fast fashion and luxury fashion alike.

When near-shored, MTM could be 45% less polluting than RTW, for the whole life cycle of the garment.

4. Impact Assessment

Which of these overproduction reduction methods can help reach the industry’s 2050 net-zero goals? Let’s compare the decarbonisation effect of MTO and MTM, with the most popular current decarbonisation method: sustainable material production (SMP). Three criteria for assessing decarbonisation effectiveness are used:

4.1 Potential Scale

What is the theoretical reach of the solution in terms of market- value, volume-, weight- and market emissions?

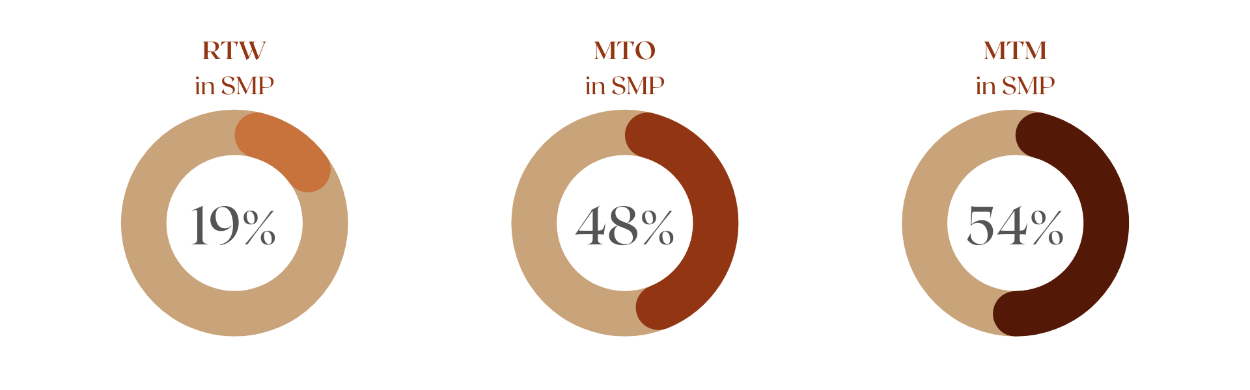

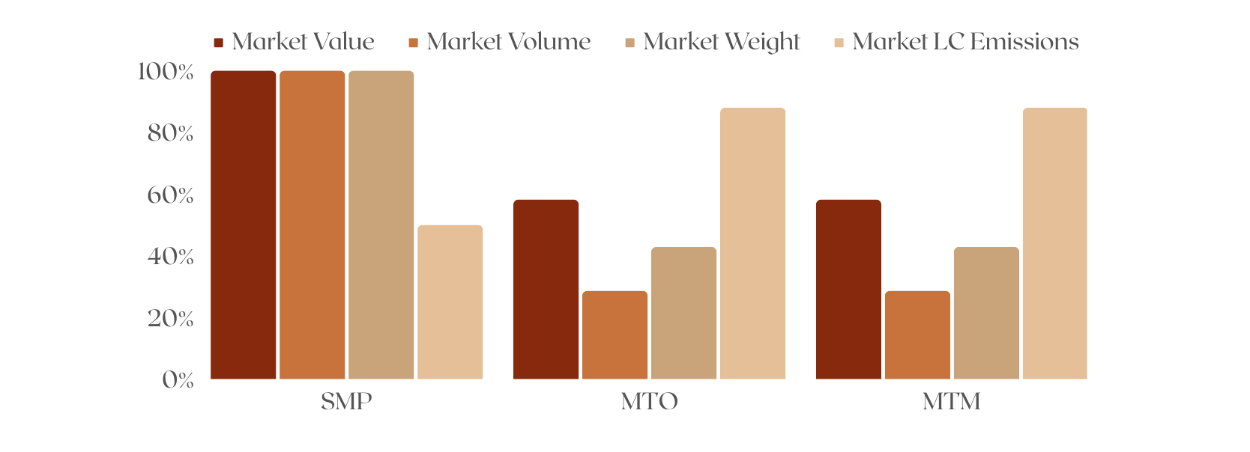

SMP theoretically affects 100% of revenue, volume and weight. MTO and MTM affect 59% of the market value, 29% of its volume and 33% of its total weight. SMP affects the production phase (44% of the emissions throughout the garment’s life cycle). Whereas MTO and MTM lower the number of garments produced, the number of garments distributed and the number of garments incinerated or landfilled, thereby affecting 83% of the garment’s life cycle emissions.

4.2 Absolute Effectiveness

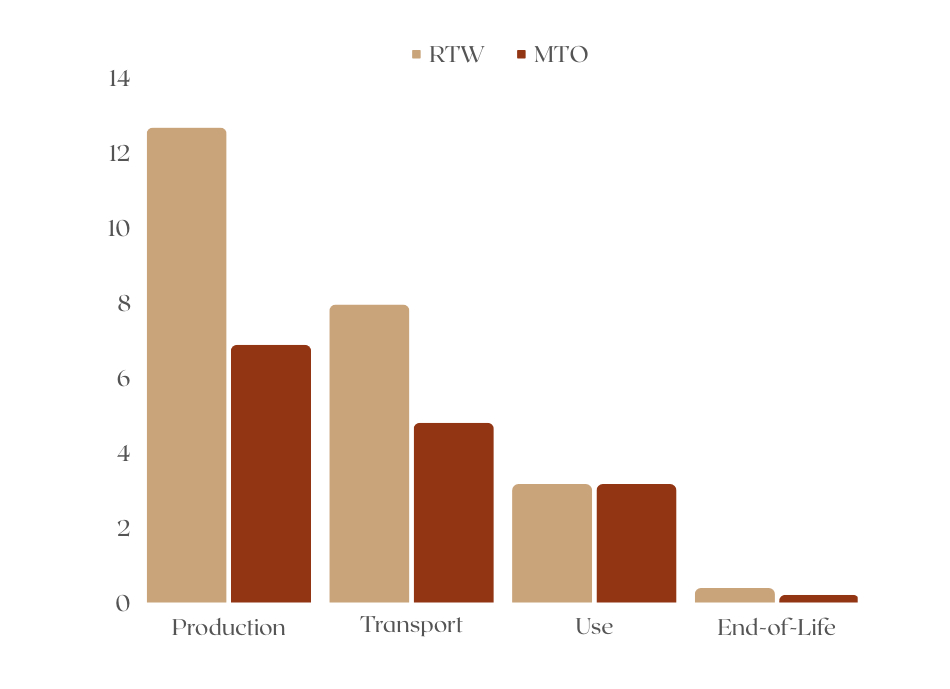

Let’s dive into the decarbonisation effect of SMP, MTO and MTM for three of the four life cycles:

4.2.1 Production Emissions

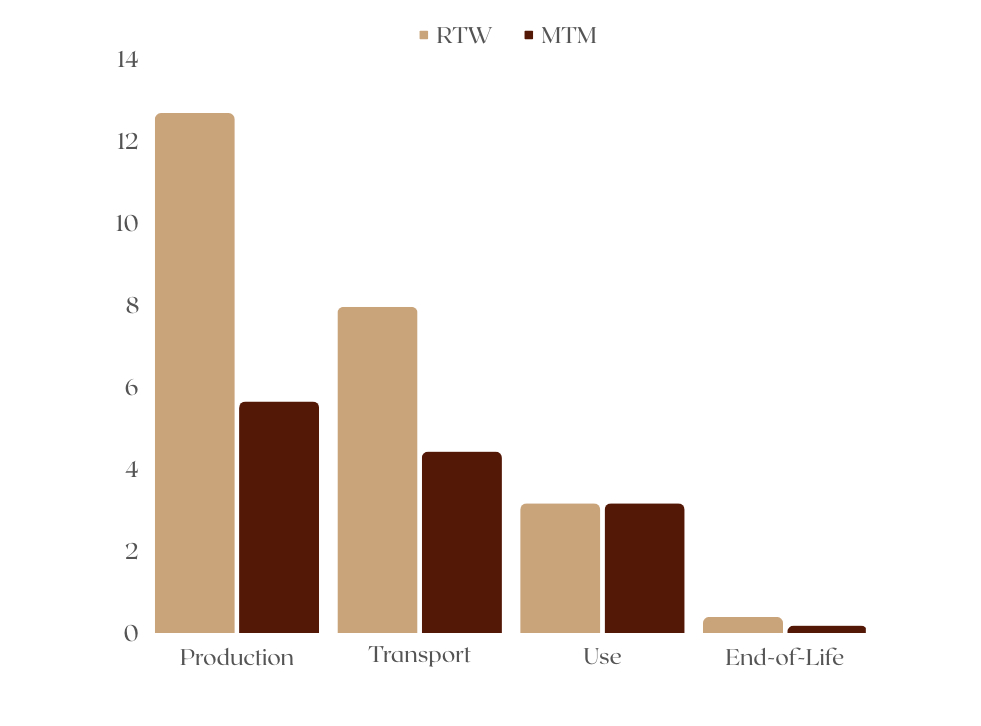

According to the Apparel Impact Institute, if brands find a way to make (material) production as sustainable as possible, projected apparel production emissions for 2030 amount to 932 billion kg of carbon. Unfortunately, the emission target for 2030 is 564 billion kg of carbon, meaning we still need to remove an additional 368 billion kg of carbon in 2030. In just the production phase. The only way to remove the remaining 368 billion kg of carbon is by reducing overall production volume. MTO and MTM can save 46%-55% of production emissions respectively per upperwear garment sold (as compared to RTW).

4.2.2 Transport Emissions

While near-shored MTO and MTM production also save hugely on the transport and distribution side of things (40%-44% per garment sold respectively), it is our hope that by 2030, the majority of transport will be done in renewable energy. This would mean that MTO and MTM would still reduce the number of garments that need to be shipped, but with zero emission shipping, their carbon reduction effect will be negligible.

4.2.3 End-of-Life Emissions

The final phase of a garment’s life cycle up until recently has been overlooked. But pictures from landfills in Ghana and Chile are printed on our collective minds. Brands need to take more responsibility and decrease overproduction and the subsequent over-destruction of unsold goods. MTO and MTM can save 46%-55% per garment sold respectively in this phase.

If brands ‘only’ optimise SMP, they could save a total 19% of carbon (for the total life cycle of the garment), as compared to RTW production in a regular material. If brands optimise SMP and produce MTO, they could save a total 48% of carbon. If brands optimise SMP and produce MTM, they could save a total 54% of carbon.

4.3 Cost Effectiveness

As important as the potential scale and the absolute effect of the decarbonisation solution is, brands also need to consider its financial ROI. Tech Tailors has published an article on the economics of MTO and MTM in 2022. We performed a similar analysis, this time focused on upperwear. We also updated our set of assumptions:

- direct-to-consumer upperwear sales

- identical production volumes for MTO, MTM and SMP

- identical (full) price points for MTO, MTM and SMP

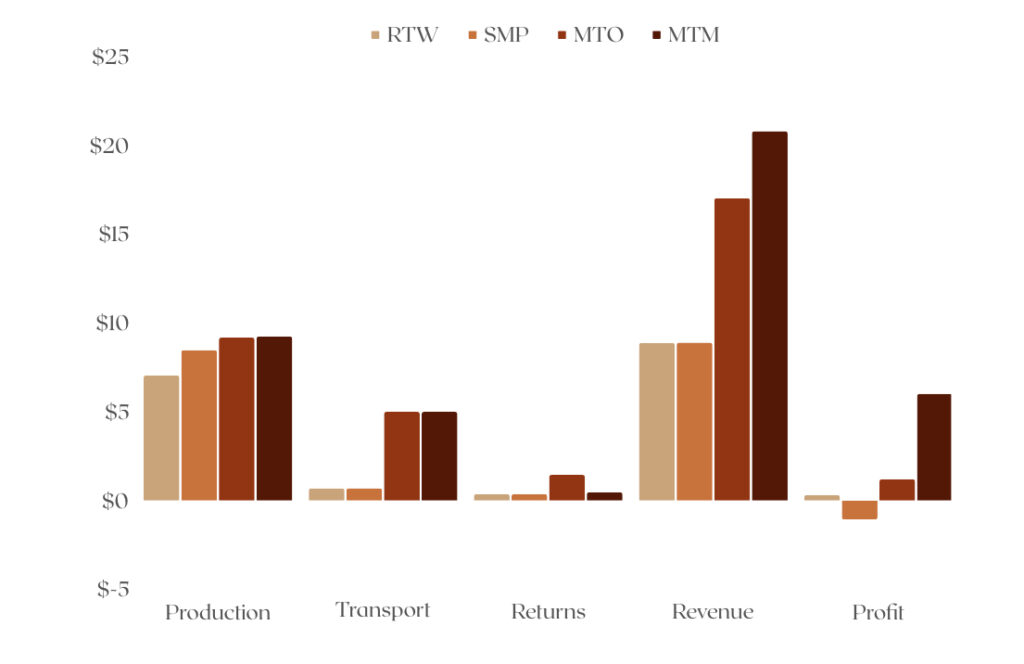

- 30%-31% higher unit production costs for MTO & MTM respectively

- 20% higher unit production costs for SMP

- 73% of sales are in store, 27% of sales are online

- returns are allowed across the board

- customers pay a $5 fee per online return

With respect to offshored RTW production in a regular material, SMP production costs are 20% higher, but at identical price points, this cost increase is not offset by higher revenue, resulting in a negative gross margin of -12% for SMP. Even though MTO and MTM production costs are 30%-31% higher than RTW, and the transport costs are seven times higher than for RTW, these cost increases are offset by the revenue increases, resulting in gross margins of 7% for MTO and 29% for MTM. These higher margins can be explained through a higher sell through rate, and the fact that all MTO and MTM sales are at full price.

MTO, MTM and SMP margins could be greatly affected if brands were able to charge a higher price point for custom, tailored and more sustainable garments. MTO and MTM garments are often sold at a ±30% higher price point than RTW in a regular material, whereas SMP garments are often sold at a ±15% higher price point. The harsh reality is that customers are often willing to pay a higher premium for customisations/tailoring than they do for a standard garment in a more sustainable material.

Conclusion

Tech Tailor’s research has demonstrated the immense decarbonisation potential of reducing overproduction. And the only way to effectively reduce volume, without sacrificing margins, is MTO & MTM.

Right now, the most efficient MTO and MTM production is done off-shore (from a Western perspective). Global production scale is estimated at 100 million units per year. But as demonstrated in the previous section, that won’t cut it – not by a landslide. The industry needs to scale up on-demand production capacity to billions of garments per year. And they need to move it closer to home.

We can no longer afford to ignore output reduction as an instrumental part of decarbonising the fashion industry. If we want a fighting chance of meeting 2030 targets, let alone 2050 targets, the industry needs to invest in SMP and MTM facilities, right now.

Besides investment, the fashion industry is also in dire need of more rigorous legislation. The EU is making a lot of headway with their ban on the destruction of unsold goods, but with 106 billion unsold garments per year, the industry really needs to get a tighter grip on this. Which starts with stricter regulations. Firstly, we need an unambiguous definition of overproduction. Something that’s quantified, but not defined, still leaves us with nothing but vagueness. The industry needs to agree on a collective definition of overproduction, with a clearly defined scope. Secondly, legislators and regulators need to force retailer’s hands by requiring them to disclose (over)production volumes in units of garments and in total garment weight in their annual reports. Only then will we know what is actually going on behind closed (factory) doors.