[Featured images: Designer Kids Club, Powered by Provenant]

Hey, and welcome back to The Interline Podcast.

If you’re a parent today’s episode might have some special resonance for you, but if you’re not, don’t skip the show just yet because today we’re gonna be digging into the luxury resale market. Not just from a practical and platform point of view, but from a perspective of trying to understand how to make the incentives for everybody align and to figure out how far those incentives can be extrapolated to serve a vision for wider, more mass market circularity.

If you are a parent, I don’t need to tell you what it’s like staying on top of a wardrobe for people whose sizing requirements change week by week and the very muddy landscape of spending money on that stuff and then trying to figure out how much of that money you can claw back. If you’re not a parent, just picture me recording this episode sat on the floor surrounded by vacuum sealed bags full of kids’ clothes and trying to figure out which ones my kids have worn, what they haven’t, what came from a hand-me-down and what’s going out to a hand-me-down in somebody else’s direction. I’m actually recording this in a booth, but that picture is still pretty representative of the buying and owning experience for kidswear.

And kidswear is the lens we’re taking today on a much wider problem because it, especially at the luxury end of the market, represents almost the ideal set of circumstances for testing and proving out the principles and the technical realities of secondary markets, of digital product passports with uncertain provenance of first party data in them, and of the need for everybody in the circle to benefit financially if circularity is going to work.

To get into all of that, I have a bit of an unusual guest today. We don’t normally talk to early stage tech companies, but there are two things I do really like doing. I like talking to company leaders who are still close enough to the product and the problem to be animated by their own first-hand experiences on the other side of the equation as consumers. And I like talking to companies that see a technology or a platform opportunity, but who feel like they need to set out to demonstrate the viability of it by building and running their own brand or retail business on top of it.

My guest today has both of those perspectives.

Mo Kharodia is the Chief Technology Officer for Designer Kids Club, which is a UK company that both sells pre-loved and authenticated designer children’s wear and is also developing and partnering to create a technology platform that they believe lines up all of those incentives for sellers, buyers, and especially luxury brands.

Let’s get rolling.

Never miss an episode

Get notifications for new podcast episodes, plus our weekly news analysis, events, and more, delivered straight to your inbox.

NB. The transcript below has been lightly edited.

Okay, Mo Kharodia, welcome to The Interline Podcast.

Thank you for having me.

Not at all. The pleasure’s on this side of the table.

So we always try and start these shows with two things. A description of what your day-to-day looks like and a definition of something.

So first up, we’ll start with the typical working day. And it’s always interesting for me to see what a CTO role, a brand or retail organisation looks like, because they can have very different scopes depending on the type of company and its objectives. So I think rolled into this one is a question about what does your day-to-day resemble and what does a CTO at a company like Designer Kids Club do?

Okay, this is going to be interesting. My day looks very different to how this all started. DKC wasn’t born as a business plan, it started at home. My wife bought our son some very expensive Burberry outfits, as you do with your first born. And within a week, he’d outgrown all of it. So we literally had bags full of clothes within the first few months. And we just sat there thinking, this doesn’t make sense. These are beautiful, expensive pieces, hardly worn. What do we do with them?

So we realised there was a gap in the market for luxury pre-loved and she very quickly built the first version of DKC. Watching that was eye-opening for me because, coming from a corporate background, I feel us men have it so much easier. As a woman building technology in fashion and from an ethnic minority background the barriers were real so I couldn’t sit back and watch that, so I stepped in and naturally fell into the CTO role. Within 18 months we rebuilt everything from a fully custom fashion tech ecosystem with the operational backbone behind it.

But despite being CTO most of my day isn’t actually spent on technology, it’s spent on system thinking – how do we make circularity work for families? How do we help brands make it profitable? And how do we connect things so it scales? Because children’s wear is the highest churn category.

Okay, perfect. Interesting background. I think anything that comes out of a first-hand need, any kind of business that grows out of a first-hand need is always an interesting one to talk about. Because there’s always that inevitable gap between the scale, which we’re to get to, and the initial kind of inciting problem. And the inciting problem is quite often one that people recognise in themselves. And I think we’re going to get to that as well because I have three kids of my own and I think I’ve been on some of this journey too.

Before we get there though, let’s do the definition side of things. The word I want you to define for me is authenticity. Now there’s a dictionary definition we could use but the more useful one I think is what that word means within the context of what you’re doing at Designer Kids Club – which I’m going to use DKC if that’s all right, just to shorten it from here on.

Now one angle at that would be anti-counterfeiting because we’re talking about, as you said, lovely expensive garments. And the other would be the lifecycle impact and circularity and the trustworthiness of the data that goes into that. You know, how authentic is the story and the provenance and the impact. And the other is the memory in the story in the other way. You know, we’re talking about clothes that children wear at vital junctures, early stages of their lives where family memories are being built.

There’s a whole lot packed into the idea of item level identity and story and things here. So, and I think there’s also your platform side of things like DKC. What level of attestation and liability you’re taking on as an authenticity provider? There’s just a whole lot. When you say authenticity, there’s a whole lot packed in there. So what does it mean to you?

It’s a great question because I don’t think authenticity is one thing anymore. Kids roll with thousand-pound changing bags now, right? It’s not just luxury exclusive for others. So for us, it’s about trust across the entire lifecycle of a product. And we’ve seen that clearly when we’ve done customer insights. So we interviewed 40 customers and 10 brands. Eight out of ten customers have bought a fake at some point and eight out of nine say trust is key before they think about buying pre-loved.

So the barrier isn’t demand, it’s trust, it’s authenticity and it’s not a small issue because counterfeiting as you’ve mentioned is a huge issue. It’s a 500 billion dollar global economy. Even brands struggle to detect it. So when we say something is authentic DKC will approve and show it. That’s why every item is physically authenticated and, for items over £100, it’s verified again through LegitApp. So using human and AI models combined. So that proof is then embedded directly into our digital product passport. So when a customer scans it, they’re seeing verified proof tied to that specific item.

And we’re already seeing how important this is at a brand level. We’ve seen brands launch brand approved resell models. That goes to show how central trust and authentication are becoming in the secondary market.

But I think the game changer here is that authenticity for us goes beyond proof. It’s about the data because a passport is only as strong as what’s inside it and we feel there’s a layer which is really important, especially in kidswear, which is memory. These aren’t just expensive clothes or everyday products. They’re moments, they’re first birthdays, they’re holidays, they’re milestones. So authenticity isn’t just about proving something is real. It’s also about preserving that story that comes with it. And when you bring those together, proof, data, story, I feel that’s when trust really builds and that’s when it lands with the consumer.

Okay, I think that’s a good definition.

Now, I’ll level with you. One of the reasons this interview made it through the pitch pile – and we do, you know, we get a lot of ideas sent our way – is that, as I mentioned, I’ve got three kids. To be clear, mine are not rocking around with thousand pound changing bags – we’re not there. But I am acutely aware of what it feels like to open a wardrobe and realise that you’ve got a rail full of hangers containing stuff that your kids have never worn and that they’ve now outgrown, or maybe they’ve worn them once or twice.

I’ve also got the typical parent thing which is a loft full of hand-me-downs, our attic for our US listeners, full of hand-me-downs going in both directions. So from other people to my kids and from my kids outwards. I have vacuum sealed more bags in the last 11 years of my life than I ever thought I would do. Turns out it’s quite hard to do! I suspect every parent listening to this is nodding along with all of that.

And that universality is also kind of behind the predicted growth of the volume of resale in kids and baby categories in general outside of luxury. I found some stats to suggest that that market beyond luxury is predicted to double to somewhere in the region of like $15 billion US by the end of the decade.

The question is, given the scale of the problem that I’m talking about here, which is more mass market, probably some premium mixed in, why pick luxury? What is it about this narrow market segment that makes it the right place to prove out what you’re trying to build versus going after kidswear in general?

I love the fact that you’re living this and you’ve lived this with the whole wardrobe dilemma because that’s exactly where this all starts. You know the moment of opening a wardrobe and realising, wow there’s so much that’s not been worn or it’s not had its best life.

Every parent can relate to it and the scale is clearly there but, for us, the starting point wasn’t scale. It was more about where does this actually work commercially? It’s got to make money sense because if circularity isn’t commercially viable, it can’t scale. And that’s why we chose luxury. And that’s why luxury is important because kidswear is not only the highest churning category in fashion, but you’ve got a constant cycle of high quality clothing being underused. And when you lay a luxury on top of that, it holds value, it lasts, it’s built to last, it carries emotional meaning. So it’s naturally suited to live multiple lives and go on and go on and go on.

So that’s why we chose luxury. Not because it’s a niche, but because I think it’s the cleanest place to start and prove the model. And we’ve already started doing that. So we’ve circulated over 5,000 items. We’ve served over 2,000 families across 30 countries. And we can’t keep up with the demand so that tells us that parents want to be able to retain value and the behaviour works when the system is there. However on the brand side resale is already happening – it’s just outside of their ecosystem. Think Gucci, Montclair, Burberry, you know their items are being sold daily on eBay, Vestiaire, Vinted so they lose customer they lose data, they lose more, they lose the relationship.

What we are trying to enable is the opposite. We want to work with brands so they can offer take back, they can stay connected, they can generate value across the lifecycle of the product.

So luxury becomes the proving ground for us because if it works here we can scale into the wider market and that’s the bigger play for us.

I’ve got two questions. One, follow up I’ll get to in a minute. The other is, if the model works because of the intrinsic value in the residual, does it break down when you get to products that are inherently less valuable?

I feel it does because financially it won’t make sense for either us, the brand or the consumer. There’s got to be a monetary value attached to it because a lot of time, energy, resource, effort goes into keeping the item in the loop. And, yeah, it’s got to make financial sense for anyone to inherit from a brand perspective or even a customer for them to be able to take a time out to send it in, etc.

It’s got to make financial sense.

Yeah, I think that’s right. And I think, as well, it’s important to put this in context because we’re not talking about a solution to fast, ultra fast disposable fashion here. That model and that behaviour pattern exists independently of the model and the behaviour pattern that brings higher quality, more durable, more sustainable in the longterm kind of garments to market.

My follow on question then is related to what you mentioned, which is, given the residual value of luxury goods, which, you know, that’s true for luxury goods owned by grownups who tend to treat products more harshly and for longer than kids do. You’re operating in a space that the luxury brands themselves might want to play, right? So these luxury brands are companies that, on aggregate, they don’t like their relationship with the customer to be mediated. And they’re also companies that sell small numbers of SKUs to dedicated cohorts of high net worth individuals.

So, for them, the secondary market is something that they know it’s happening – Vinted and Vestiaire Collective and so on – they know that third parties are doing this. At some point, it feels like they would want to do it for themselves. It feels like the incentive is there for them to own that channel to the consumer. And the scale of the problem is not unmanageable in luxury. If you’re a luxury brand, you don’t have huge volume, huge variety and so on.

What is it that you see as your potential kind of moat as one of those sort of intermediaries? Is your advantage in the tech layer? Is it in the curation layer? Is it in the storytelling? Is it something else that I’ve overlooked?

Yeah, I think you’re right. Luxury brands do want to own that relationship. And in the long term, they probably will. The challenge is, and the reality is, they’re not set up to do it today. And that’s really where we sit. Our mode is the infrastructure layer that we’ve built to make circularity work at scale. You can already see the direction of travel. Brands like Gucci have trialed resellers, Selfridges launched to resell for several years ago, Ralph Lauren recently has built its own vintage and resell model where they actually buy from other platforms. And that makes up 10% of their annual revenue now. So the intent is there, but it’s still very fragmented.

And that’s because when you look at how brands operate, even something like a simple return is actually very complicated. Their tech stacks aren’t built for multi-lifecycle ownership. They’re often on legacy systems or use platforms like Shopify which are great for selling products but not actually managing complicated infrastructure or managing a product over time.

Let’s take something like resale pricing like an AI evaluation. Something like that still takes Vestiaire Collective 2-3 days. We can do it in seconds at DKC using AI and take the same for authentication on marketplaces like Vinted. It’s an additional step, you know, a customer has to buy a product, they’ve got to send it into a hub. It’s then actually authenticated and then distributed out to the customer. For us, we’ve built that in by default. So the experience is faster, trusted in real-time.

So resale looks simple, but operationally it’s one of the hardest things to execute. And that’s why I feel brands won’t be able to do it themselves tomorrow. And most initiatives stay stuck in pilot because it’s not the idea that’s wrong. It’s operationally very difficult.

We are not trying to own the customer. What we are trying to do is enable the brands to own the lifecycle. We connect the intake authentication, pricing, everything within our system with a value flowing back to brands and customers. All we’re doing is in that way it still feels native to luxury.

So that’s what makes us different to marketplaces, you know, they’re peer-to-peer and the responsibility sits with the user. But what we’ve seen is that customers don’t want the hassle of resale. They don’t want to deal with the effort and the energy involved in being able to resell. So we’re not building a marketplace. We’re building the supporting layers and the infrastructure underneath it. Because once you solve that, once we make resale or any circular initiative seamless and we can measure it, value doesn’t disappear after the first transaction it lives on.

That’s a good answer. And I’ve kind of got two following comments to it. One would be, I think you’re right that the brands will want to own it eventually. I think there’s also a tipping point where they have first-hand business units to deal with. Their business is primarily based on linear new product introductions and selling those through, which means that the secondary market for them is a secondary consideration by default. I don’t mean it’s unimportant. I mean that it cannot secure the same level of investment as their first-hand business models can. And there will be a ceiling on how much time and effort and capital they funnel into those kinds of initiatives until they feel like they can be at least on roughly equivalent footing to their first-hand business model. So there’s that point and other things.

Now, you mentioned AI a couple of times, and I think I want to find out specifically what you mean. So it sounds like you think you have an advantage from the product ingestion and authenticity and assessment and everything else point of view that is AI native. Tell me what that means.

Yes, so we’ve built AI into everything from back-end operations to front-end to actual consumer features. So, the authenticity – being able to link that back into the DPP, being able to give a real-time value using AI, being able to see how quickly an image is degrading over time if a customer is adding multiple photos into the DPP. We use different models for pretty much everything and I feel that’s what gives us the advantage.

It’s allowing customers to have an enhanced experience, like our AI model, which we’re currently building, which we’re refining, will be automatically able to recommend products that customers own in their digital wardrobe and create outfits from pre-loved wardrobe inventory and suggest other pre-loved items that would potentially go with it. So if they have a birthday party on the weekend, they have a fancy shirt and they have a pair of jeans but they’re missing shoes, our AI model will be able to recommend based on the profile of the customer the right pair of shoes from the DKC ecosystem.

So that’s kind of where we’re playing, and I think the digital wardrobe is a very important enabler of us being able to make pre-loved the first option when considering a new purchase.

Okay. And just because we’re working on our AI Report for this year at the moment, and we’re talking to a couple of companies that consider themselves to be new and AI native. Do you think there’s a version of what you do that can exist without AI or do you define yourself as an AI native company as well?

I think we’re hybrid. There are some things technology and AI can’t solve and you know it’s a manual process or it’s very complicated so there are limitations but when it comes to scaling and optimising there’s a lot AI can support us with. AI is an enabler, it’s a tool, it’s not an actual end-to-end solution so that’s why I go back to hybrid where we’re building a technology ecosystem that combines a series of tools and technologies to facilitate the circularity of luxury kidswear and beyond – but it’s an interesting space I think.

The only thing I’d like to say is that everything we do as a brand is customer-centric so if a customer has told us or multiple customers are telling us something and we explore it further and we find there’s a need for it there’s an opportunity for it we then go and invest in building out what we found is that customers wanted not only proof of verification but they wanted real-time valuation. They don’t want to wait three days to see how much a product is worth. They want to know now, is it a good time for me to sell? You know, baby Joe’s outgrown it. I need my next Moncler jacket. I don’t want to buy a brand new one for £600. I’m happy to buy pre-loved. Can I get rid of this one and buy the next one? Gen Z is very different. They’re very financially savvy. They’re clued up. They’re very smart and they kind of transact in a very different way where they want to experience, you know, they value experience over traditional ownership as such.

I think that makes sense as a lever on the scaling side of things. To use your product label here, so tell me how Relux Story, which is the DPP (Digital Product Passport) initiative that you have going, tell me how that works from the QR code to the platform. How are you binding a physical item to a digital passport entity? What portal or front end does the consumer interact with, the user, guess, in this case? And what does the backend infrastructure look like?

Did you entertain any other approaches to physical tagging using NFC or anything like that? Tell me what that bridge between the physical item and the digital representation looks like.

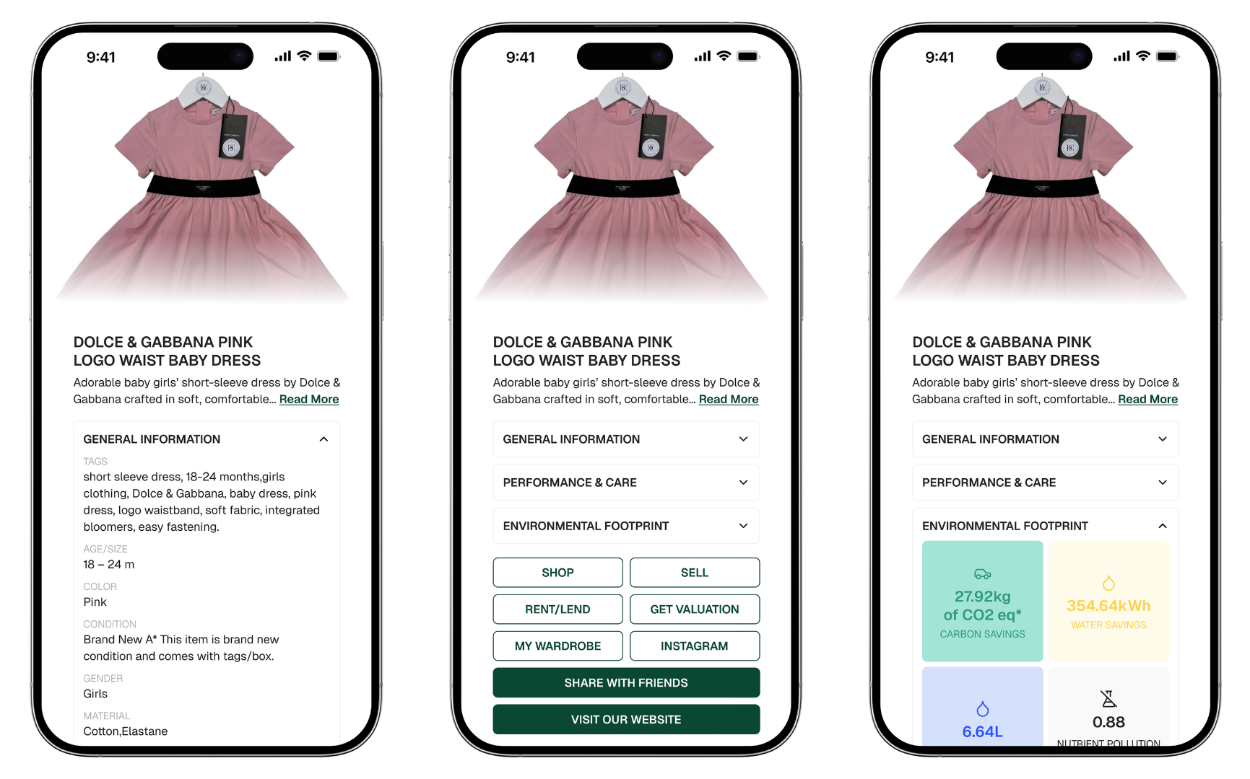

Yeah sure, so I’ll keep this simple from the outside and then we’ll go into like the deeper layer. At a customer level every garment that comes into the DKC ecosystem has a digital identity that lives in its digital product passport, so when a customer scans a QR code on the garment or opens it in their digital wardrobe they’re not just seeing their listing, they’re seeing the full digital profile that includes everything: the product details, care advice, impact metrics, authentication and in the future lifecycle events like the journal.

So where it gets really interesting is how that’s all connected. So every physical item is bound to a unique digital record and that is at the point it enters our system. So we create that passport in real time via API and it becomes a persistent identity that stays with the product across its lifecycle.

In the back end we’ve kind of built this as a lifecycle system, not a transaction system. So instead of buying an item and it being sold and reselling, it moves through multiple states over time. So ownership, resale, condition changes, it’s all tracked within the same identity and we’ve obviously touched on authentication and how we bind that into the DPP.

So in terms of tagging we started with QR codes because they’re simple and they’re scannable. And we’ve explored NFC for higher value items, but the key isn’t the tag itself. It’s the connection between the physical product, the physical version and its digital twin. And importantly, we don’t rely on the customer to scan every time. Most interaction happens through the digital wardrobe where we can prompt the customer at the right moment of time, for example, a good time to resell based on our AI insight because once that connection exists and it’s relatable to the customer those products become unstatic then they become trackable they’re transferable assets and that’s what Relux Story is about. It’s not just adding information for the sake of it but it’s about making every product ready for its next life from day one.

OK, and that was one of the things I wanted to ask about. So, one of the ideas that grabbed me from your announcement was the notion that a garment can be “resale ready” from day one. Tell me what that means, how it fits into your vision for this being a platform that brands adopt, and what you think the incentive is for luxury companies to approach it that way?

I’m glad that stood out because that’s the idea. That’s the idea that sits at the core of what we’re trying to do. Today, most products are designed for a single life. You buy it, you wear it and then everything else resets. Resale has become separate. It’s a manual process that the customer has to figure out. Hey, what do I do with this? Is this something for vintage eBay? What platform? Facebook.

What we’re saying is that that shouldn’t be the case. Resell ready from day one means a product is set up for its next life the moment it enters into the system. So it has a digital identity, authentication is attached, the data starts building in real time immediately. So instead of a one-time transaction it becomes an asset that moves through multiple lives and that matters because what we’re seeing from customers is families have high value items, barely worn. They don’t want the hassle of selling. They want a fair value back and they want an easy way to move on to the next item. So the behaviour is there. The system just hasn’t caught up.

For brands, there’s an opportunity here. Instead of selling once and losing visibility they can offer take back. They can stay connected to the product. They can retain the customer relationship. They can continue to generate revenue beyond its first sale. So resale stops happening outside of their ecosystem and becomes part of the core business model and that’s the shift here. And once you do that you don’t just enable resale you enable a system that actually works at scale.

Okay, I think that’s a good summary. That’s well captured.

Now, when we think about digital product passports in either the kind of casual definition or the straight sort of legal definition, we’re talking about a container with a standardised form rather than a prescriptive list of what that container necessarily needs to hold. And that means that the container is only as good as the data that goes into it. And in the case of pre-loved secondary market items, that means that the data is only as good as the original brand was willing to make it or was able to make it.

And I’m going to use a specific case study here. Earlier this year, Prada, is one of the luxury labels that would be present on DKC, confirmed that they’d had to sever ties with more than 200 of their Italian suppliers and subcontractors after an audit found non-compliant conditions in a bunch of different ways. I think overall that’s something like more than a quarter of the suppliers they expected failed, and similar supplier scrutiny has also affected other luxury companies, Dior, Valentino and so on.

Long story short, if digital product passports had existed for garments that were produced underneath those operating conditions and those supply chain structures, the value of the data contained in that digital product passport would be questionable because the brand that attested to it then later had to walk that attestation back effectively. Your role in that scenario is downstream of whatever methodology the brand uses.

How do you approach this challenge of being able to say that we can track the lifecycle and the impact and the story of this garment, but you’re beholden to the information that the brand provided in the first place and sometimes that information isn’t as robust as we’d like it to be.

Yeah. This is a very fair challenge and I think it’s one the industry has to be honest about. You’re absolutely right, a DPP is only as good as the data that goes into it and today that data isn’t always complete. Supply chains are complex, even brands don’t have full visibility. And we’ve seen with the cases that you’ve mentioned involving Dior, Armani and Valentino, it all shows how difficult it actually is to maintain full transparency, especially across global supply chains.

So the idea that DPPs could solve that overnight isn’t actually realistic. You know, we take a very pragmatic approach. We focus on what we can control within our ecosystem and what we can verify. You know, that means standardising the data we can independently, verifying key elements like authentication with partners like LegitApp and then making that transparent product level.

So, beyond that, we treat the DPP as something that evolves. For us it’s never been a static record. It becomes a living profile. As the product moves through its lifecycle we add data. We can verify that directly. Ownership, condition, repair, resell, events, even the stories behind it. So trust doesn’t rely on a single point in the supply chain. It builds over time and I think that’s the reality of the shift from trying to create perfect data upfront to building systems that improve the data and transparency progressively. Because the industry isn’t starting from a perfect place, but doing nothing isn’t an option.

So we’re not trying to solve the entire supply chain issue. What we are doing is building the infrastructure that allows better data, better trust, better accountability to exist at scale. And over time, naturally, as systems grow and adoption increases, creates the right conditions for brands to improve as well because transparency and the customer consumer expectation starts to drive that change. And I think ultimately that’s how we as an industry move forward, but we do have a lot to do.

And I think that’s a really great point. It’s becoming clear that people, consumers, don’t necessarily want to buy sustainable garments in the new market. There’s a lot of proof points out there to demonstrate the fact that people don’t put as much money, well, they put a lot of personal emphasis and individual value emphasis on environmental sustainability and then they don’t back it up with spending.

However, when you look at the secondary market, I think you have a consumer that’s already conditioned to want sustainability. You have a consumer that’s already conditioned to want transparency, because they’re choosing to buy used rather than to buy new. And you’re already through that gate. And then I think as that community expands and as that market expands, I think you’re right. I think that does create the conditions for the brands to improve the data that goes into the products when they’re new, to improve that lifecycle impact assessment.

Because if these are products that are going to have longer lives with an audience that cares about what went into them in the first place, that’s a very different set of incentives to just selling things new to a consumer that might not care.

So your partnership with Provenant is interesting. So Provenant, if I understand it, is the technology layer underneath the Relux story side of things. There’s a quote from the CEO of Provenant where he’s talking about the idea that there’s a difference between digital product passports as a compliance exercise and digital product passports as an opportunity to innovate. I broadly agree with that. I think there’s definitely a bunch of companies who see DPPs as a checkbox and something to just get past. And then I think there are some that see it as a chance to build something new. I think the regulatory weight is a lot of what’s got people moving forwards. But the innovation is what’s going to keep it going.

I’m keen to see what kind of innovation opportunities you think that you want to build on top of that. Is there anything we haven’t already talked about?

Provenant have been a really strong partner for us on the innovation front. They’re genuinely forward thinking and I think what stood out was that they’re not focused just on compliance. They focus on building consumer facing features that actually align with where the industry is going and what consumers want. So we did speak to a number of providers, but we felt they were very much checkbox-driven. Provenant had a clear vision and that roadmap aligned with where we want to go in the future, which is why we partnered with them.

And I think I completely agree with Lars. Vision, like regulation, is what’s getting the industry moving? But if DPP stays a compliance exercise they’ll never deliver real value. Customers won’t use them. It has to be more than a checkbox exercise, they’re the foundation for the new layer of fashion and fashion experience. Because once you give it a digital identity it stops being something you just sell and it becomes something you can manage, track, see and build over time and that’s where the innovation starts. Instead of asking what data we need to store we’re asking how does that build trust like how does that make resale seamless, how does that extend the relationship between the brand and the customer? And that opens up a lot of opportunities.

Products are resale ready from day one – we can track how they move through multiple lives, can price intelligently, brands can offer take back. So there’s that whole experience layer and we’re turning something meaning into something more meaningful. And that’s the real shift. So the DPPs go from being a static record to becoming something very dynamic, something consumer facing, something that drives the behavior change that we want to see in the industry.

So compliance gets you started but I think the innovation and the change is what makes it valuable long term.

Penultimate question. Designer Kids Club described itself as a circular fashion ecosystem rather than a marketplace. And I think we’ve already described, you’ve done a good job of capturing it, you’re not a marketplace. We’ve already talked about your ambition to make that ecosystem available to other companies for them to plug into. We don’t normally do a second definition, but I think it’s relevant here. What does a circular fashion ecosystem actually look like when it’s put into practice? What is the ideal version?

Yes. So, DKC started out of frustration as I’ve mentioned, you buy something nice, the kids wear it a handful of times and suddenly it doesn’t fit and you’re left staring at a wardrobe thinking, what am I actually supposed to do with all of this? Sell it, deal with messages, chase people, you know, no thank you. So what we built is basically the system we wish existed. For families, we take that effort away. We handle the resale. We handle the pricing, the logistics, and we actually get value back for them, for the things that they’ve bought instead of them just sitting there.

So in practice, it’s really simple. You request a DKC Relux bag, you fill it up with the items you’re done with, you send it in from there. We handle everything, authentication, curation, repairs, pricing, know, resale, rental, logistics, sale. On your side, it’s all tracked in your digital wardrobes. As a consumer, you can see what’s happening with your items from day one. Has it been sold? Is it being marketed? Have I received any earnings from it? Usually we pay a commission between 50-90% and they can opt for a cash or a brand credit payout. So this becomes an ongoing cycle without the usual hassle. Hey, I need to take photos. I need to upload it and Vinted needs to check my messages and so forth. So for brands, it solves a problem they’ve always had, but never really owned. Right now, once they sell a product, they lose visibility, their customer, the future value. So instead of clothes being worn once and forgotten, we help to keep them moving from one family to the next.

And what I think I’m getting here and I don’t necessarily disagree with it is the idea that a circular ecosystem industry-wide, if we were to say what would it look like for fashion to go circular in a broad sense it has to have a financial component to it – it has to have a value component to it for all of the people that exist in the circle. Not just for the original brand, not just for the marketplace holder, not just for the consumer. Everybody has to stand to benefit. Everybody has to have a stake and everybody has to have an incentive to keep something moving in a circle. Otherwise, its natural inertia makes it fall out of that circle.

Yeah, I agree. It’s a triple aim for a brand, consumer, for planet. Everyone’s got to benefit financially, otherwise it doesn’t make sense. And I think that’s what we’ve tried to do with DKC, where we’ve been realistic and reasonable and pragmatic about how we make this work financially. We’re not saying that consumers are going to be able to recover 100% of their original investment, but they get a very good proportion of what they paid for an item, the brands get a very good value retention, we financially are rewarded, so it works and I think without the financial incentives, without the financial incentives to exist for any one of those parties it just won’t work.

Yeah, I think you’re right. I think people are economic actors first and foremost, and then they’re principled and personal actors thereafter.

My final question is related to this a little bit behaviourally. So we haven’t done, at The Interline, a Sustainability Report for a couple of years. You’re testing my memory, but I think 2023 was the last time we did it. And that’s not because we lost interest. It’s because the market seemed to go into a bit of a period of paralysis for a while. There were legislations being redefined, reframed, reprioritised, brands and companies reprioritising or reevaluating their investments in sustainability and transparency tech initiatives. For a period, it seemed like nothing was really moving and people were hesitant to throw what they maybe saw as good money after bad if the regulations and the consumer behaviour wasn’t going to evolve to make it necessary.

Do you think we’re on the other side of that now?

Because your bet is that brands see value in this in the long term. Do the brands you trade in and the partner conversations you’re having with brands suggest that the industry now recognises that it still has a mandate for change that hasn’t gone away and that there’s now more drive to put that into practice maybe than there has been for the last couple of years?

Yeah, I think what we’ve seen over the last few years was never a loss of intent, the intention to become more sustainable and circular has always been there. But it’s reset. So if you look at the wider industry, it’s under real pressure. High street stores are collapsing. Brands are downsizing, they’re diversifying into things like hospitality, cafes and real estate. So it’s a highly competitive market and everyone’s fighting for margin and relevance.

So the reality is, while sustainability is often talked about as a priority, when it comes to actual implementation decision making it has to make commercial sense and that’s why things have slowed down.

What we’re seeing now is a more honest phase. From our customer insight, sustainability on its own isn’t the primary driver. Parents care about value, convenience and trust first. Sustainability matters, but it’s like an add-on. It’s a bonus. It’s not the reason they act and not the reason why they’ll choose pre-loved. So brands are in a similar place. You know, it’s high on the agenda from a reporting perspective, but investment only happens when it makes sense.

So the question has kind of shifted from should we do this to does this actually work as a business? And we’ve seen where it can work like Polo Ralph Lauren and their buyback. So, you know, that’s where circularity starts to make sense. So the brands are moving now. They’re moving and they’re doing it for optics. They’re doing it because they can see the upside in retention. You know, they can see the new revenue streams. They can see the better use of products over time.

On the consumer side the behaviour has always been there but the experience was broken: too much hassle, too less trust, or not enough value return so you end up with this gap where the demand is clearly there, the pressure exists but the system hasn’t caught up. And that’s why I do think we’re on the other side of that slowdown, on the other side of that pause, it’s because we’re in a different phase now. It has to be easier, it has to be valuable, it has to be commercially viable for all actors involved because that’s what actually changes behaviour and that’s what makes circularity scale at every level whether you’re on the board, you’re an investor, the brand, the consumer, the decision still comes down to economics.

Yeah, that’s a really good answer. Thank you, Mo, this has been a good conversation. Thank you for being willing to entertain my questions. I’ve got a lot out of this.

Thank you for joining.

Thank you for having me in. I really appreciate your time.

And that’s the end of my chat with Mo.

This was an unusual one in that we don’t, as I’ve said, often talk to companies at this stage of their journey. And circularity feels like such a big topic for a smaller player to take on. But I meant what I said earlier in the conversation: tech companies that emerge out first-hand need are often the ones that end up making a difference, or at the very least, they’re the ones that have the most interesting perspective on what needs to be done.

And there’s that big idea that I want you to take away from this show, which is that we talk about the financialisation of everything in a negative context. Or at least, I certainly do. But when it comes to the sweeping scope of behavioural change that would be needed for fashion to genuinely go after circularity, those financial incentives just have to exist, and they have to be universal.

As always, next week we have something completely different, so keep an eye out for that. And don’t forget to submit your questions for our mailbag episode, which we’re doing at some point soon. You can email me directly at editor@theinterline.com. You can send me a direct message on LinkedIn, and pretty soon we’ll put up a short survey on the website to kind of capture questions from people as well.

For now, thanks for listening, and I’ll talk to you again really soon.