[Header images courtesy of unpsun.]

Welcome back to The Interline Podcast. We’ve talked about domestic manufacturing on the show before. Back in 2025, I interviewed Nick Reed, the Founder of a sustainable menswear brand here in the UK called Neem London. We covered a lot of ground in that episode, but the part that stuck with me was him saying he hadn’t been able to do a full ‘made in the UK’ collection despite wanting to, because the infrastructure he needed as a brand owner wasn’t there — and he didn’t think it would be there unless something dramatic happened.

The kind of dramatic we were talking about was, realistically, a leap forward — or sideways — in manufacturing technology, or government support in the form of sponsorship and subsidies that would let in-country producers pivot to a different model. We’ve also talked about leaps in upstream technology recently, when Stephen Bates, the CEO of Rheon Labs, joined me in June. He and I discussed how hard those leaps are to make, and why so many innovators flounder when it comes to translating a novel concept into a viable commercial proposition.

Here at The Interline, we’ve written extensively — along with plenty of other outlets — about the conditions creating a really strong mandate for the kind of state-level investment in domestic infrastructure that will be required for brands to feel confident placing orders, and for manufacturers to have the stability to support them.

You know those conditions. It’s tariffs. It’s wars. It’s the general shakiness of the global order. Today’s guest has thought about all of this extensively, and has seen it from both sides of the curtain. Arne Arens has been a top-flight brand executive: he was Global Brand President at The North Face from 2017 to 2021, then CEO of Boardriders — which owns Quiksilver, Billabong, Roxy and DC Shoes — and a board member at Everlane. Earlier this year, Arne moved into technology, joining 3D weaving company unspun as its CEO.

If you listen to this show for long enough, you’ll know that CEOs are some of my favourite guests, because they either have a genuinely broad vantage point and an understanding of everything under their remit, or they don’t — and it becomes obvious very quickly where there’s a hole. Arne is firmly one of the former. He gets every side of this discussion in a way that only someone who has led a brand and now runs a technology company deep in the weeds of production can — and he was game for me querying him on basically all of it.

So let’s hear what he had to say.

Never miss an episode

Get notifications for new podcast episodes, plus our weekly news analysis, events, and more, delivered straight to your inbox.

NB. The transcript below has been lightly edited.

Arne Arens, CEO of unspun, welcome to The Interline Podcast.

Thanks so much for having me, Ben. Pleasure to be here.

We always start these shows by trying to pin down what the guest’s day-to-day role looks like, and I think yours might be the closest thing to catnip for our fashion technology audience that we’ve ever had — because you’ve made the lateral step from the top flight of some highly recognisable brands, North Face and Boardriders, into probably the most dynamic and volatile stage of a technology takeoff: the point at which a venture-backed innovation goes through industrialisation and commercialisation. We’ll come back to how you ended up in tech and what drew you here. But right now, tell me how your time is divided. How much of a typical week or month is spent on factory floors with machinery, in meetings with development teams, visiting partners, or working to get unspun’s Vega platform embedded into the supply chain?

It’s a great first question, and it’s very different from what I did in my prior roles. Right now it moves a little from month to month, but it’s roughly a third, a third and a third. A third of my time is with commercial partners — brands and manufacturers — in their offices and in our own factory building, because we like to show our machinery and our tech. That’s really where you see it come to life.

A third is capital fundraising, which is part of any startup — and I include the work we do with our board in that. We’re a deep-tech company in the industrialisation phase, and that phase is very capital-hungry, so it’s a pretty much permanent part of the job. The final third is internal: engineering reviews, reviewing test plans with the team, operations, hiring, and maintaining the culture we have at unspun.

What’s really exciting for me since joining unspun is that everything is so tangible. We have a micro-factory in Emeryville. The machines are here. We start the day with a 9am stand-up with the whole team. When I was at North Face or Boardriders, the product was made nine thousand miles from my desk. Here, I can watch a pair of trousers come off the machine before we get our day going. That tangibility changes the way you run a company and interact with the team. It’s really concrete — and that’s the part that excites me.

It’s a very unusual thing for a tech company in particular. A lot of people are accustomed to working on software, which is ephemeral by nature. So you’re in a very unique position there.

Exactly.

The second thing we ask guests to do is define some terms — and you’d be surprised how often asking someone to pin down a seemingly simple term gets them talking about it from a different angle.

I want to take a term everyone’s familiar with and add a word that will probably leave people with a much less clear picture. Everyone listening is comfortable with what a woven fabric is, and everyone’s familiar with ‘3D’ in a few senses — geometry, mesh and texture design, additive manufacturing, 3D printing, maybe 3D knitting, because I recently interviewed Garrett Gerson, CEO of VARIANT3D, and people have some experience of seamless knit constructions like Nike Flyknit uppers. But 3D weaving is a different prospect.

So walk us through it: what exactly is 3D weaving as it’s embodied in unspun’s Vega, and what makes it interesting enough that someone in your senior brand-leadership position would be swayed to come and work on it rather than staying on the brand side?

As your audience knows, the apparel market effectively consists of woven and knit fabrics — roughly 50/50. On the weaving side, traditional weaving makes a flat fabric. The way it’s been done for decades, maybe longer, is that you take that flat fabric, cut shapes out of it, sew them together and create a final product. All the things that are challenging about apparel manufacturing live in the multitude of steps you have to go through: the waste on the cutting floor, the labour in the sewing, and the lead time — because, thanks to the cost of labour and labour arbitrage, most of that has moved to Asia over the last couple of decades.

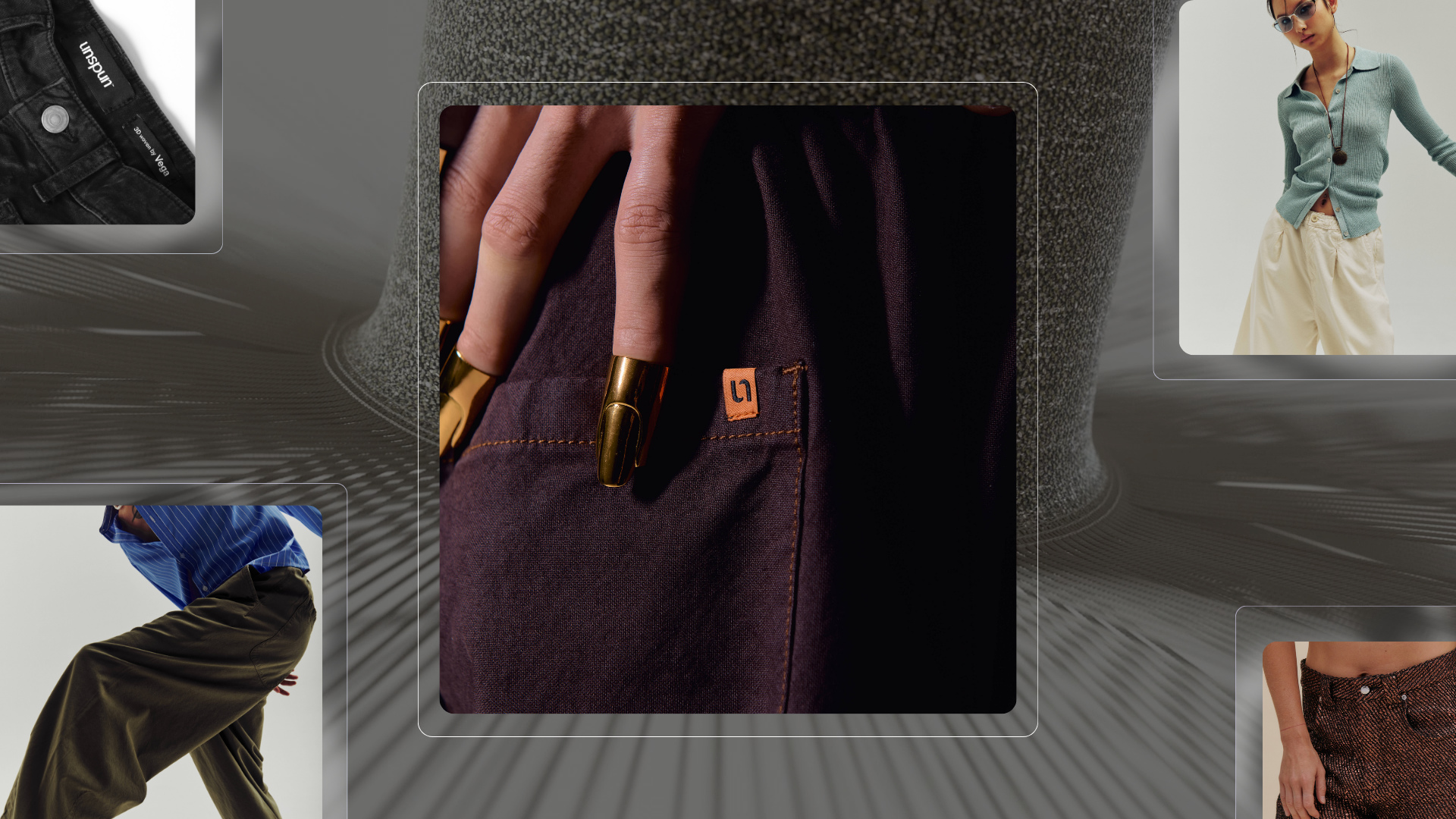

What we do is different. We have a machine we call Vega, and it weaves the shape itself. Thousands of individual yarns — we have 3,000 yarns — go into a loom that interlaces warp and weft directly into a seamless three-dimensional tube. The weft is woven in a circular motion, and that creates a tube, which in our case is a trouser leg. It can also change geometry and diameter as it weaves — wider where it needs to be wider, more tapered where it needs to be narrower. So there’s no cutting. The result is a pair of trousers that is effectively seamless, which is pretty unique, because that hasn’t been done before in a woven space.

It’s a woven cloth, so you get the structure, the hand and the durability that make a woven a woven — but it’s completely seamless, and it’s made from yarn to final fabric in one step through the loom. That’s the marrying of weaving and 3D. It’s different from 3D knitting, particularly in the speed of the process: 3D knitting is relatively slow, which so far has kept it at relatively high price points and made it niche. We can do a pair of trouser legs in about eight minutes, which means we can run this process at scale and at cost.

That’s part of what convinced me. I’ve spent the last twenty years on the other side of this supply chain, and I’ve seen everything that’s challenging about it — long lead times, huge complexity. Over the last couple of years it’s only become more fragmented: it started with the pandemic, then geopolitics, and more recently tariffs. Supply chains keep fragmenting, and there’s real risk in them. Because our system is effectively on demand and can be done locally — you can put machines in Europe or the US and make to order — you cut out a lot of the lead time and a lot of the inefficiency.

Having seen the challenges of the old way of doing things, being part of something that revolutionises it and addresses so much of the financial waste, the large carbon footprint and the environmental waste that the legacy system creates was just really exciting to me.

We’ll get into the scale and the ease of deployment in the US or anywhere else. I don’t think I’d realised you had a low-cost play here as well. In my head, when you hear ‘innovation’ — in production, in materials, in finishing — you automatically attach a rider that says this is now a premium product, something that has to amortise its cost by the final product being expensive. It sounds like that’s not the ambition here.

No, it’s not — and that’s what’s unique about this technology. Obviously it’s a very innovative new technology with a clear consumer benefit: seamless trousers, which are more comfortable garments. But the fact that we can do this at cost and at scale means the labour arbitrage that was the main reason for putting production into low-wage countries goes away. We can now economically and feasibly do production in the West. Our main target markets are Europe and the US, because the lead-time reduction — which is the core benefit of our system — comes to life best when you’re close to the consumer.

I want to ask about unspun’s history, because I’ve been familiar with the company for a while — I interviewed your CTO, Kevin Martin, on stage in Paris once, and Beth Esponnette, your CPO these days, has written for us at least once.

I’m testing my memory here, but in the earliest days I remember unspun being outwardly a brand, producing custom-fit jeans — that’s how a lot of people first knew it — while inwardly it was a technology company using that consumer-facing brand to prove its vision and test its technology. Nowadays the brand has served its purpose and you’ve broadened the remit onto everything we’ve talked about: bringing manufacturing back to the US and to Europe. In the US in particular you’ve got letters of support from some of the country’s biggest retailers — REI Co-op, Walmart. I know the brand part predates you, but you’re well embedded in the culture now.

Tell me what’s remained consistent from that initial founding pilot — that brand experiment — to where you are today, talking to some of America’s biggest retailers. That feels like a very big journey.

It’s a great question. What’s absolutely stayed intact is the core conviction that you should make a garment only after you know someone actually wants it — not nine to twelve months out. One of the biggest challenges with the current supply chain is that you have to order nine to twelve months ahead, so you invariably get a lot of it wrong, and there’s a big gap between supply and demand. That’s where a lot of the financial — and environmental — waste comes from. When unspun started by making a pair of custom-made jeans for you, it played on exactly that thesis: we produce after someone has indicated they want it. That on-demand model has stayed the same.

What’s different is the model around it. We’ve pivoted from being a direct-to-consumer brand — with a website where you order custom jeans — to a technology company selling machines to manufacturers around the world, so they can benefit from the technology, the reduced lead time and all the efficiency we bring. Instead of ordering nine to twelve months out, you can order one to two months out — a 70-80% reduction in lead time. That’s huge, and it cuts so much waste and inefficiency out of the supply chain. Different model, same core conviction.

It does make sense. The undercurrent of what you’re saying is that if you produce on demand — if you can cut 70-80% out of the lead time — it changes the kind of brand you can be. And that’s the sort of thing you only really know once you’ve tested and proven it yourself. Almost every brand is structured around that nine-to-twelve-month lead time; it’s baked into how they operate, and it carries through everything — design, development, sourcing, production, marketing, advertising. Cut a big portion of that out and you can be a different type of company. You don’t just get to be the same company but faster. To me that’s a really important unlock for any kind of domestic on-demand production.

I think you’re 100% right. All of a sudden there are shorter-term trends you can play on, rather than having to predict everything nine to twelve months out. That’s a completely different way to approach your business.

Reshoring in America specifically carries a different weight today than it did even a couple of years ago. You’ve mentioned tariffs; there’s a lot of geopolitical upheaval, and all of it is combining to light a fire under the idea of ‘Made in America’ — which is clearly a tailwind for what you’re doing. Do you think those conditions will last? Automated, on-demand, domestic manufacturing sounds very appealing right now. Does that appeal survive the outward conditions changing back, where offshore production becomes slightly more favourable again? Or is there more to the macro picture than just hedging against whatever’s in the mind of the current US administration?

Our idea lives independently of that. It’s obviously been a giant tailwind, because it’s only made the case for reshoring bigger — the fragmentation of supply chains, plus the financial implications of tariffs on top, has made the case for ‘Made in America’ or ‘Made in Europe’ stronger. But the core of our business is reducing lead time, and that holds regardless of how high the tariff is or where your original production sits. Being able to produce locally and on demand is uncoupled from tariffs. If they went away and it became economically feasible to produce in China again, the nine-to-twelve-month lead time still applies if you do it the old-fashioned way in China, versus our one-to-two-month lead time if you do it with unspun in the US or Europe. So we’re experiencing a tailwind right now, but our business model doesn’t depend on tariffs staying in place.

We’ve talked about the preconditions of the model in America, and you’ve hinted at Europe a few times. Some of the conditions you’re describing are geopolitical and unique to America, but a lot of what’s endemic to fashion — overproduction, long lead times, material and process waste — is just as much an issue in Asia and Europe.

How portable do you think the unspun model is? What do you believe you need to accomplish domestically before you take the vision to Europe — or are you ready now? How many domestic hubs in the US is enough for you to say the economics and the lead-time benefits are demonstrated, and this is a model that can work anywhere?

The model could work anywhere right now, and the reason I say that is that the labour arbitrage goes away. The financial benefits of the unspun model come through two things: automation — you no longer need people to cut and sew — and the inventory-forecasting benefit that comes from lead-time reduction. Our model is financially feasible in the US because of those two factors, and it’s equally feasible in Europe. In fact, Europe is probably a little easier, because wage rates in Turkey and Portugal — the number-one destinations for apparel production in Europe — are already lower than in the US. So if the model works financially in the US, and it does, it certainly works in Europe. We’re already there.

Right now we need to build up these manufacturing hubs in the US, and to do that we’re partnering with both brands and manufacturers to create a triangle — between ourselves, brands and manufacturers. We marry demand from brands to the manufacturing capacity that manufacturers bring to the table, with our technology in the middle. It already works financially today, so we’re ready to go.

So that’s the 3D weaving machinery, and its deployment into the supply chain internationally. Let’s talk about the software and the ecosystem too. When you describe an innovative production method like weaving in a tube, the traditional design paradigm — 2D and 3D CAD — is to design pattern pieces that are then assembled afterwards. This is a different way of doing things.

I wrote a piece back in 2021 — it took me a while to find it again, because five years is a long time in this space — where I talked about the vision for something like a CDN, a content distribution network, which is how images get served to you from the data centre closest to you. I was thinking about an asset-first approach to design and production: product creation and design centralised and done digitally, with localised, distributed nodes doing the manufacturing. Back then I was picturing cut-and-sew micro-factories, because that’s what I knew, and the handoffs from design, development and PLM to CMT partners are pretty well established. What you’re doing with unspun sounds close to that vision made flesh — but you’re using very different hardware in the nodes, which presumably requires a different software approach for product design and development to feed it.

It does. But the core idea is pretty close to what you were thinking about five years ago. The big difference is that the last step — into what you’d describe as the manufacturing nodes — is now effectively our tech. We’ve built a layer of software on top of our 3D weaving machine that tells the machine what to do, and it connects to what brands and designers are already doing by translating whatever a designer does in CLO 3D into something the machine can read. There are two layers to that: a CAD layer that translates the design into a digital version, and then the machine software — the firmware — that translates that into what the machine actually does.

In our model, the garment really becomes a file. The product is designed and engineered digitally — the 3D geometry, the weave structure, the construction — and that definition compiles down to a machine instruction. You can send that file to any node, and the machine produces exactly that same garment.

So there’s no requirement to buy new specialised software, the way there might be if you were working in knitting. You can take the existing talent and the software ecosystem you’ve built up in CLO, for instance, and you’re not having to rip and replace it.

That’s exactly right. It’s seamlessly translated into the layer of software that sits on top of our machine and tells it what to do.

We recently did a show with Stephen Bates, CEO of Rheon Labs — an ingredient technology for energy control, which has partnered with Decathlon and others. He and I talked about what I’ll glibly call the graveyard of upstream innovation, and how to avoid ending up buried in it.

We’ve seen a lot of companies in ingredient technology, fibre inputs or production innovation start with a flashy pilot, or sign a deal with one halo partner or a research institution, and then collapse when the rubber hits the road — when commercial reality means scaling and delivering a worthwhile return.

Correct me if I’m wrong, but you’ve said unspun is ready to go, ready to slot this platform into the supply chain. Are there any hubs built out and running at capacity yet? What’s your read on the challenges between where you are now and where you’re aiming to be — and what can you do to avoid ending up where those other upstream innovators have?

We obviously don’t want to end up in that graveyard. We’re starting from a really strong foundation: our micro-factory in Emeryville, where we have seven machines. A couple are used for R&D and a number for full production, so we know the tech is ready for deployment. That’s the first thing. Our primary model is selling machines to manufacturers, and those machines slot into their existing production systems. There will be some changes versus how they do things today, but it’s an add-on to their current setup. On the other side, we partner with brands that buy garments from those suppliers — usually the suppliers they already buy from — so we slot into existing commercial relationships. We don’t ask either brands or manufacturers to bet on a startup or a vendor with zero track record.

Secondly, we’re maniacally focused on our industrial metrics. We hired Andy Hamilton, who came from Tesla and Redwood Materials, and his whole mantra is uptime, repeatability and quality yield — all validated in our own micro-factory in Emeryville. We create the production conditions there before we ship a machine, so there’s a very rigorous framework around deployment readiness. And, as you referred to, we’ve signed agreements with a number of large manufacturers and retail brands, here and in Europe, marrying manufacturing capacity with demand from brands. The intent is to build those first manufacturing hubs in the US and in Europe.

When I spoke to Kevin on stage in Paris a couple of years ago, we got into the idea that you need a different framework for evaluating the value of producing in-country and on demand than the one you use for offshoring. We’ve talked about labour arbitrage and time saving; the essence is that looking at unit cost alone ignores a lot about where profitability and risk actually come from. That said, people are very much in a unit-cost mindset — it’s how brands are conditioned to think about production. As part of announcing some of those partnerships, you’re aiming for a 400-to-500-basis-point gross-margin improvement for brands, as well as the reduction in time to market. We’ve done the time-to-market point to death. Where does that extra margin come from? And crucially, how much of the way brands currently think about forecasting, planning, pricing and planned markdowns needs to change for them to get that kind of return?

t’s a great question, and it goes to the heart of what we do best. The lead-time reduction I’ve been banging the drum on is directly related to the gross-margin uplift. Right now, an average apparel retailer discounts around 40% of its units on a seasonal basis. It starts early in the season with low discounts, and they rise as you head towards the end-of-season sale — but in general, say 40% of units go at some level of discount, let’s call it 30% off. A lot of that comes from the inherent mismatch between supply and demand when you have to order twelve months out and make an inventory forecast. I’ve lived this for twenty years — it was the biggest challenge we faced every single season, both on the balance sheet and the P&L.

If you reduce that from twelve months to one or two, your forecasting accuracy goes up, and that 40% gets closer to the industry best. Take Zara: they’ve got the system figured out, at least on the part of their supply chain made close to home in Europe, and there they discount around 15%. So if, instead of 40%, you now discount 15% of your inventory at 30% off, that alone is around 400 to 500 basis points. On top of that, if you don’t pay tariffs and don’t pay transport because you’re producing locally, that’s additional gross margin we haven’t even factored in. So we’re very confident the business case for a brand is very accretive.

We’re equally confident about the manufacturer — we work with both sides of the triangle. For a manufacturer, the automation and the collapsing of six or seven steps into one lowers material cost, because you don’t weave flat fabric, ship it elsewhere, then cut and sew; it all collapses into a single step, which cuts materials cost by 50-60%. Add the automation of the process, and over four to five years a manufacturer can double its margin versus the legacy supply chain. So it’s 400 to 500 basis points at minimum for brands, and a doubling of operating margin for manufacturers. And I haven’t even mentioned that, because we cut out overproduction, transport and production waste, the positive environmental impact is very significant too. A study we did a couple of years ago indicates it’s around half the carbon footprint of the legacy supply chain. So both financially and in carbon terms, the savings are substantial.

So there are benefits to brands and benefits to manufacturers. That’s particularly interesting because, to realise those mutual benefits, somebody has to go first. Presumably Walmart, REI and the others signed those commitments because they see the potential returns, and the manufacturers you’re working with see the same. But those letters don’t contractually lead to purchase orders or volume commitments.

So what are the next steps to go from partnerships of principle to reliable POs? When I think back to conversations with brand owners here in the UK about domestic production, the biggest barrier they mention is that local manufacturers don’t have enough reliability and consistency on their order books to switch models — at least without government support. I know it’s different in Portugal, where there are subsidies to support micro-factories.

It’s a bit of a chicken-and-egg problem: brands struggle to place on-demand orders through infrastructure that isn’t there yet, and manufacturers struggle to bet on building that infrastructure without forecastable, predictable demand. To be blunt: at what point does this become viable for both parties, so people can make decisions and forecasts based on something tangible?

You’re hitting the crux of what’s important for us at this step. As we deploy machines into the world, we have to marry demand from the brand side with supply from the manufacturer side — that’s the great balancing act, bringing the three nodes of the triangle together. Right now we’re seeing really good traction. We’re in advanced conversations with Arvind, a vertically integrated apparel manufacturer in India that potentially has its eye on the US at some point too, though the first step with them would be in India.

They work with the largest brands in the world — Gap, Levi’s, PVH and so on — so they’re a world-class manufacturer, very innovation-minded and very sustainability-minded, and they’ve got their eyes on our technology. The other corner of that triangle is a Japanese brand, Muji, which has done advanced sample development with us; we’re in the final stages there. That’s one leg of the stool.

Second, we’ve been doing work with Walmart, whom you mentioned earlier. We’re in advanced stages of sample development with them and connecting them with a manufacturing partner in the US — which, by the way, is not an easy task, because there isn’t a lot of apparel manufacturing left in the US, as you know. But there are parties that are very advanced and very interested. As you’ve probably seen, we’ve put out a statement about our intent to build a facility in New Mexico, where the state government is putting a lot of support behind bringing advanced manufacturing back. So, to your point on government subsidies, this is one of those areas where we could potentially use it. That’s the second route: a US hub with Walmart as the base, supplemented by REI and some of the other brands we’ve signed MOUs with.

The third leg of the stool is that we’re lining up a number of pilots from our Emeryville hub. We have machines that can run production at very high reliability and speed, and there’s no reason not to use them. We’ve had conversations with brands like Filson and Patagonia, and we’re talking with J.Crew and Banana Republic, part of the Gap family. Those runs aren’t huge, but they’re low-risk ways for brands to step into our technology — to see that it works, see the quality, sell through with their consumers, and see that there’s uptake. That can lead to larger orders later. So there are multiple ways we’re getting around that chicken-and-egg problem. It’s real — but there are several ways we’re approaching it right now.

You talk about creating skilled American manufacturing jobs — and presumably similar roles in other markets if the model expands into Europe. I want to know what kind of jobs they’ll be.

When we surveyed a hundred professionals this year for our AI Report for 2026, the data showed that nearly half of companies have reduced headcount, either as a direct result or a corollary effect of investing in AI. AI isn’t the same technology as what we’re talking about here, but the reason I raise it is that people reported specialist skills — pattern-making, 3D expertise — being on the chopping block, not just admin or merchandising.

So any ambition to not just protect but actually net-create specialised manufacturing jobs sounds like a positive step. At the same time, part of me feels the level of automation with something like unspun risks tipping into the cliché where people say a lot of you will be replaced by robots, but we’ll keep some of you on to maintain the robots. It’s a cliché for a reason. Tell me what you think the manufacturing jobs of the future that unspun helps sustain and create look like.

To underline your point: the jobs we’re creating in Europe and the US are jobs that left decades ago. Anything we create locally is net new to the garment industry, because there aren’t any right now — we’re bringing them back. Are they the same jobs the legacy supply chain employed? No. They’re textile technicians, maintenance people, quality engineers — genuinely skilled industrial roles, with industrial wages. These are not entry-level minimum-wage sewing jobs.

And the skills your survey shows potentially being replaced — pattern-making, 3D — are exactly what we need more of. Every garment we make has to be fully engineered digitally before a single yarn moves, so pattern knowledge doesn’t disappear in our world. It becomes more important, and it moves into the product file — and it becomes more valuable, because the file effectively is the machine instruction. So we hire for those skills, and they need to keep being part of the ecosystem we create. It’s a net add of new and interesting jobs that aren’t being AI-ed away.

That’s a good answer. Final question: if all this works out, domestically and internationally, what do you think apparel production for woven garments specifically looks like a decade from now?

It’s a great question. With technology like ours, the single biggest metric that changes is overproduction. We’re moving towards an on-demand, custom-made model. If you marry what we’re doing now with the original premise of the company — personal fit — those two things lead to a custom-made, on-demand manufacturing model that cuts out any kind of overproduction. So we go from a mass-manufacturing model to a custom-made, on-demand one, done locally.

How many hubs is that in the US? One on the East Coast, one on the West, one in the middle — or thirty-five throughout the country? Or is it even more distributed? The original premise of 3D printing was that everyone would have a printer in their house. That never really happened, and it may not happen for apparel either — that might be a step too far. But it illustrates the point: there’s a distributed model around on-demand, custom manufacturing that isn’t there today but will be, and our technology is one of the facilitators. I think that’s going to be a fundamental change to how apparel is made ten years from now versus today.

Perfect. Well, if I’m still doing this ten years from now, I’ll bring you back on and we’ll see how it went.

Arne Arens, thank you so much for joining me — I’ve really enjoyed this conversation.

Really appreciate it, Ben. Thank you so much, and good luck.

And that’s the end of my conversation with Arne. As I said at the top, he’s someone who has been extremely close to a problem for a long time on one side, and is now hands-on with what he believes is the solution on the other — and I think that shows.

I hope you enjoyed it as much as I did. As always, thanks for listening, and I’ll be back with a very different guest next week, I’m sure.

These head-to-head interviews are still my baby — I love doing them every Thursday. But if you fancy something a bit lighter, a bit easier to fit into your morning commute, check out The Edit, our quickfire news-analysis show. It comes in under twenty-five minutes, it’s a more relaxed, conversational format, and it comes out every Tuesday, right here — you don’t need to subscribe to a separate feed, it’ll show up automatically. Whichever one you listen to — or if you end up liking both — thanks for being here, and I’ll talk to you again really soon.